By Giosetta Belperio

Buying your first home is one of the most important financial decisions you’ll ever make—and in 2026, the Greater Toronto Area housing market requires more preparation than ever before. While the path to homeownership may feel complex, today’s first-time buyers have access to better tools, clearer information, and more strategic options than in the past.

This guide is designed to help first-time home buyers in Toronto, Vaughan, York Region, and across the GTA understand the process clearly—so you can move forward with confidence, not pressure.

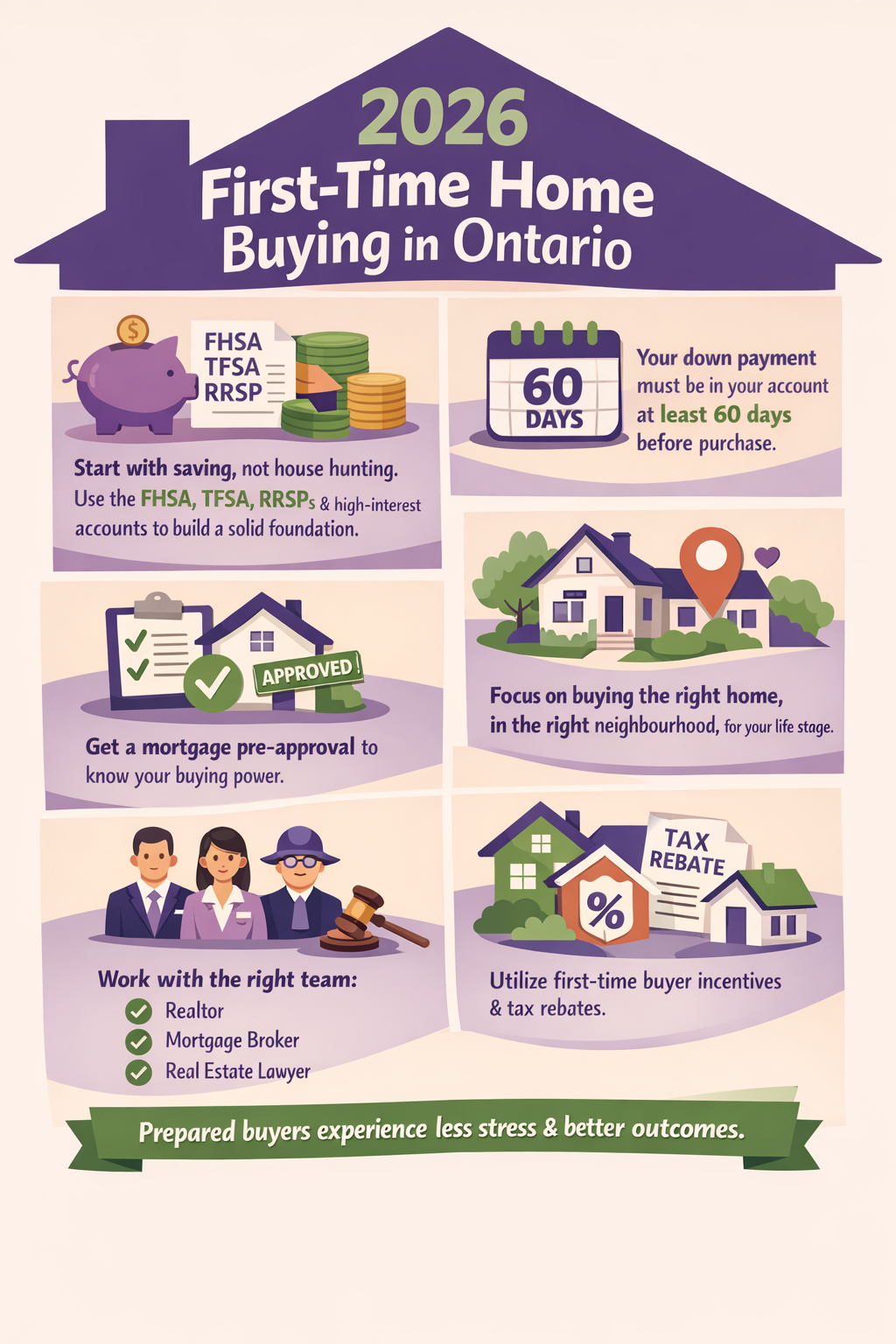

1. Start with Saving: A First-Time Home Buyer Foundation

Before mortgage pre-approvals, showings, or offers, the real starting point is how you save. In 2026, successful first-time buyers are intentional about building a financial foundation that supports both the purchase and the first years of ownership.

Saving for a home today means using the right accounts, understanding timelines, and preparing for more than just a down payment.

Key Savings Tools for First-Time Home Buyers

First Home Savings Account (FHSA)

The FHSA is one of the most valuable tools available to first-time buyers in Ontario. It allows you to save up to $40,000 toward your first home, with tax-deductible contributions and tax-free withdrawals for a qualifying purchase. Many buyers across the GTA use the FHSA as their primary down payment savings vehicle.

Tax-Free Savings Account (TFSA)

TFSAs remain essential for flexibility. First-time buyers often use them for closing costs, moving expenses, furnishings, or as a financial buffer after purchase. Because withdrawals are not taxed, TFSAs offer accessibility without penalties.

Registered Retirement Savings Plans (RRSPs) and the Home Buyers’ Plan

If you already have RRSP savings, the Home Buyers’ Plan allows you to withdraw up to $60,000 toward your first home. This strategy works best when used carefully, with a repayment plan and long-term financial goals in mind.

High-Interest Savings Accounts (HISA)

High-interest savings accounts are useful for short-term savings, especially when funds will be used within the next year. While not tax-advantaged, they provide stability and easy access. Visit your bank’s website for more details.

Why Saving Comes First

Did you know? You down payment needs the be in your bank account 60 days prior to purchase.

Mortgage lenders look beyond totals—they look at patterns. Consistent contributions, responsible account use, and clear separation between savings and spending demonstrate readiness long before you apply for a mortgage.

Starting with a structured savings plan helps first-time buyers:

Understand a realistic price range

Reduce financial stress during the buying process

Prepare for closing and ownership costs

Enter the mortgage process with confidence

2. Mortgage Pre-Approval for First-Time Buyers

Once your savings strategy is in place, the next step is mortgage pre-approval. This turns preparation into buying power and gives you clarity on what lenders are willing to offer in today’s market.

In 2026, lenders typically review:

Income stability and employment history

Credit score and debt-to-income ratios

Existing financial obligations

Down payment source and savings behaviour

While a credit score in the high-600s or above often qualifies for better rates, approvals are based on the overall financial picture—not a single number.

Mortgage pre-approval also strengthens your position when submitting offers, particularly in competitive GTA neighbourhoods.

Tip: Working with a mortgage broker and comparing multiple lenders often leads to better long-term terms—not just lower interest rates.

3. Understanding Housing Market in 2026 (Without Trying to Time It)

Many first-time buyers worry about “timing the market.” In reality, success in Toronto, Vaughan, and York Region comes from buying the right home, in the right location, at the right time for your life.

Home prices continue to fluctuate based on:

Interest rate changes

Inventory levels

Neighbourhood-specific demand

Transit and infrastructure development

Instead of reacting to headlines, informed buyers focus on:

Recent sale prices rather than asking prices

Neighbourhood-level trends

Open houses to understand true market value

Choosing the right neighbourhood is just as important as choosing the home itself. Transit access, lifestyle fit, schools, and long-term growth potential should all factor into your decision.

4. Why the Right Real Estate Team Matters for First-Time Buyers

Buying your first home is not a solo process. Having the right professionals in place makes a measurable difference in both outcome and experience.

Your team should include:

A real estate agent experienced with first-time buyers

A mortgage professional who explains options clearly

A real estate lawyer who protects your interests

In a market as detailed as the GTA, guidance, communication, and transparency are essential. The right team reduces risk, saves money, and eliminates unnecessary stress.

5. First-Time Home Buyer Incentives in Ontario (2026)

Government programs continue to support first-time buyers across Ontario. Some of the most impactful include:

First Home Savings Account (FHSA): Save up to $40,000 tax-free

Home Buyers’ Plan (HBP): Withdraw up to $60,000 from your RRSP

First-Time Home Buyers’ Tax Credit: Claim up to $10,000

Ontario Land Transfer Tax Rebates: Up to $4,000, with additional rebates in Toronto

GST/HST New Housing Rebates: Available for eligible new builds and major renovations

Each program has specific eligibility rules and documentation requirements. Reviewing them early helps ensure nothing is missed.

For a full list of tools, links, and buyer resources, visit the Buyer Resource Page.

6. A Calm, Supported Path into Homeownership

Buying your first home should feel informed and empowering—not rushed or overwhelming. Whether you are just starting to save or preparing to make an offer, my role is to guide you with clarity, honesty, and strategy.

From early planning to neighbourhood selection, negotiation, and closing, my focus is on helping you make decisions that support your long-term goals—not just today’s market conditions.

Thinking About Buying Your First Home?

If you’re planning to buy your first home in now is the right time to start preparing. Whether you have questions, need guidance, or want a personalized plan, I’m here to help.

Reach out anytime—your first home deserves a confident, well-supported beginning.